Top Ten Instrument Companies – Then and Now

This year marks the 30th anniversary of the publication of SDI’s first Global Assessment Report in December of 1989. This was our first attempt to provide a comprehensive look at the entire analytical instrument industry. The spiral-bound tome weighed in at a trim 136 pages plus appendices. Over the ensuing 30 years, we have expanded the scope of the report many times in terms of technologies covered, and simultaneously expanded the presentation to offer new kinds of segmentations and ways of evaluating these markets. Now, even in the more compact presentation style of the report, the 2019 SDi Global Assessment Report runs to nearly 1100 pages. The report is the gold standard for assessing and understanding the markets of all of the 80+ life science and analytical technologies contained inside. But the spiral binder has long since been consigned to the dustbin.

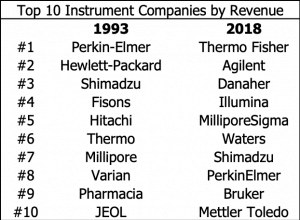

I thought it would be interesting to look at how the market participants have changed over the decades-long span of the reports. Acquisition and consolidation has obviously had a marked effect on the supplier situation over that span of time, so it’s interesting to

Hewlett-Packard is second on the list. This is more straightforward as HP’s instrument group was spun out as Agilent Technologies in 1999. Agilent still holds the #2 spot in our current rankings, helped in part through the acquisition of most of the business of Varian, #8 on the very first list.

#3 Shimadzu is also a relatively straightforward story, currently at #7. Two other Japanese companies, #5 Hitachi and #10 JEOL are also quite recognizable today, though both have slipped from the top ten into the teens in the full Top 50 list in the 2019 edition of the report.

The instrument group of #4 Fisons was sold to #6 Thermo Instrument Systems in the mid-90s. After many more years and deals, Thermo Fisher Scientific rules the roost on our scoreboard.

#7 Millipore sounds a great deal like MilliporeSigma (the US & Canadian name of Merck’s Life Science business), which now ranks at #5 in the industry. But one important difference is that in 1993, Waters was a division of Millipore, but was divested the following year. In its own right, Waters now stands at #6.

The last of the original top ten is Pharmacia, a business that merged with Amersham, which then folded into GE Healthcare. Of course, the biopharma business of GE Healthcare is expected to be sold to Danaher (currently #3 in the industry) before the end of the year. Looks like our top ten list will be rewritten once again for 2020!