Looming IMO Standards a Driver for Oil and Gas Instrument Market

Sulfur compound (SOx) discharge is one of the most regulated pollutants in every industry, as studies have shown that it is harmful both for humans and the environment. A study on health impacts associated with the delay of MARPOL global sulfur standards conducted by the Finnish Meteorological Institute in 2016 estimated that if the marine sector does not reduce sulfur content in marine fuels by 2020, air pollution from ships will contribute to more than 570,000 additional premature deaths globally between 2020 to 2025. Furthermore, SOx emissions trigger acid rain, which is harmful to crops and causes ocean acidification. For these reasons, reducing the limit for sulfur in marine fuel will have a measurable impact on human health and the ecosystem, especially for those who live close to ports and major shipping routes.

To curb these effects, the International Maritime Organization (IMO) established a new regulation, the IMO 2020, which will be globally implemented on January 1, 2020. This new regulation cuts down the sulfur content in marine fuels from 3.5% to 0.5%. The rule aims to have a 77% lower sulfur emission from the marine sector by 2025. The IMO 2020 also allows alternatives for shippers who are not able to adhere to the 0.5% sulfur limit. One method is to install exhaust gas cleaning systems (scrubbers) in ships to reduce sulfur emission. Another option is to use a “cleaner” fuel such as LNG or methanol to replace high sulfur fuel oils.

As demand for bunker fuel reached 3.5 million barrels per day in 2018, this change in regulation will certainly have an impact on the global fuel oil market. High demand for low sulfur-content fuels will lead to a price jump. Shippers and fuel sellers will begin stocking up low sulfur fuel oil while existing refineries are not quite ready to supply such high demand. Higher prices will encourage low-sulfur fuel producers to crank up their production and expand their low-sulfur production capacity, which in turn, will invigorate the oil industry in general.

With rapidly growing demand for low-sulfur fuels, the need for sulfur measurements will also greatly increase in the near future, leading to higher instrument sales for relevant techniques, including x-ray fluorescence (XRF) and elemental analyzers. The lab-scale version of these instruments will see more applications in contract testing labs and other governmental testing facilities, as flag states and port states have rights and responsibilities to enforce IMO 2020 compliance. Meanwhile, process scale elemental analyzers will see more demand from refineries, as some oil companies are investing to increase their low-sulfur fuel oil production capacity. XRF and elemental analyzers are commonly used to test for trace elements such as mercury, sulfur, nickel, metals, carbon, hydrogen, nitrogen, and vanadium in fuels.

Though IMO 2020 may cause an increase in operational costs for shippers and freight companies, it presents an opportunity for the oil industry and the accompanying analytical instrument market. In fact, this dynamic is only one of the many variables affecting the ups and downs of the oil & gas industry.

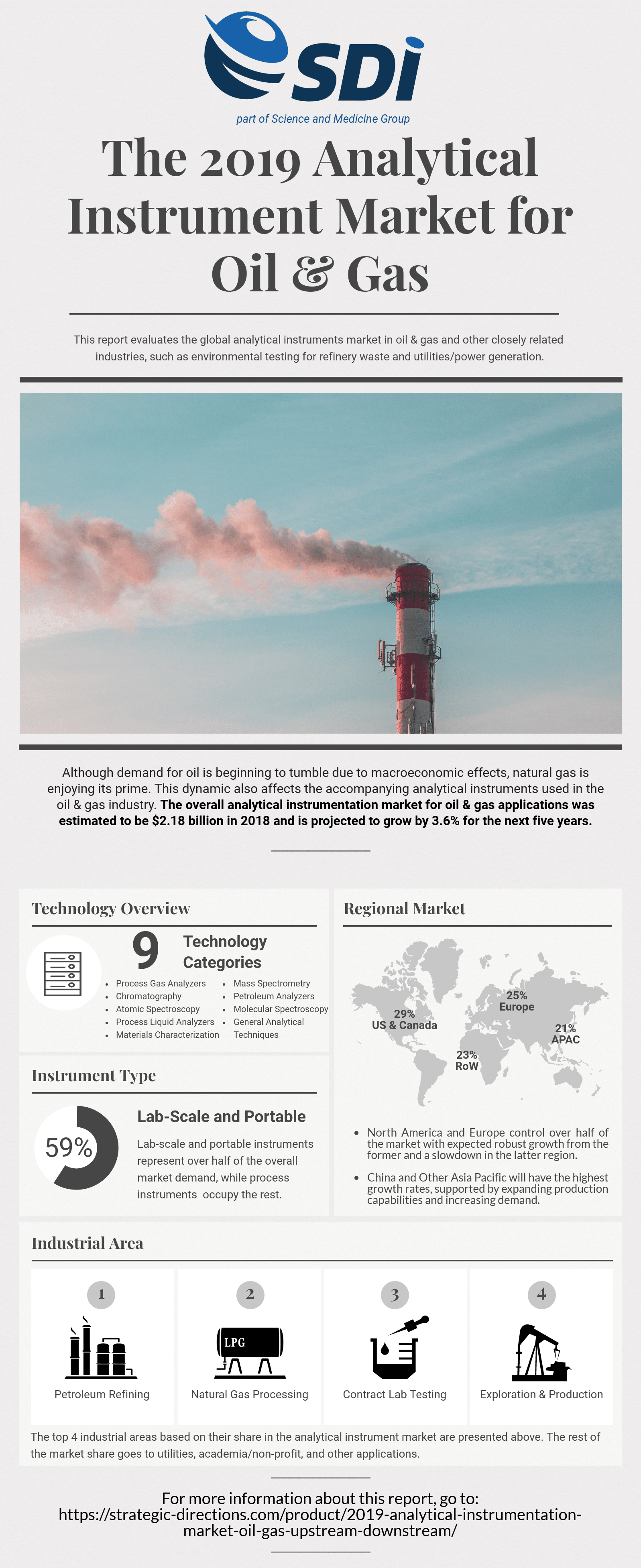

A deep dive into this complicated field can be found in SDi’s newest report: The 2019 Analytical Instrumentation Market for Oil & Gas: Upstream & Downstream. This report evaluates the global analytical instrument market in oil & gas and other closely related applications, such as environmental testing for refinery waste and utilities/power generation. It covers 48 different technologies of laboratory benchtop, portable, and process-scale instruments that are commonly utilized for oil & gas testing. The infographic below provides an overview and some highlights: